The study of Financial Astrology involves looking for correlations between planetary events and changes in sentiment in financial markets. Often the analysis involves reading angles from star charts (an ephemeris) and performing complex geometric calculations while searching for relationships.

GannTrader is a unique software module in the Financial Astrology world. It’s built on algorithms first used by NASA’s Jet Propulsion Labs. GannTrader uses these calculations to provide you with simple-to-use indicators and charts that unlock possible relationships. With a rich history and deep expertise in the field, we have meticulously developed a robust suite of tools that have consistently proven their worth over decades.

Gone are the days of grappling with complex calculations and deciphering intricate charts. GannTrader gives you a modern, intuitive platform that enables you to effortlessly navigate the realm of financial astrology. Built on the powerful Optuma financial analysis platform, the user-friendly interface and sleek graphics provide crystal-clear visibility into your results, ensuring you stay focused on what truly matters.

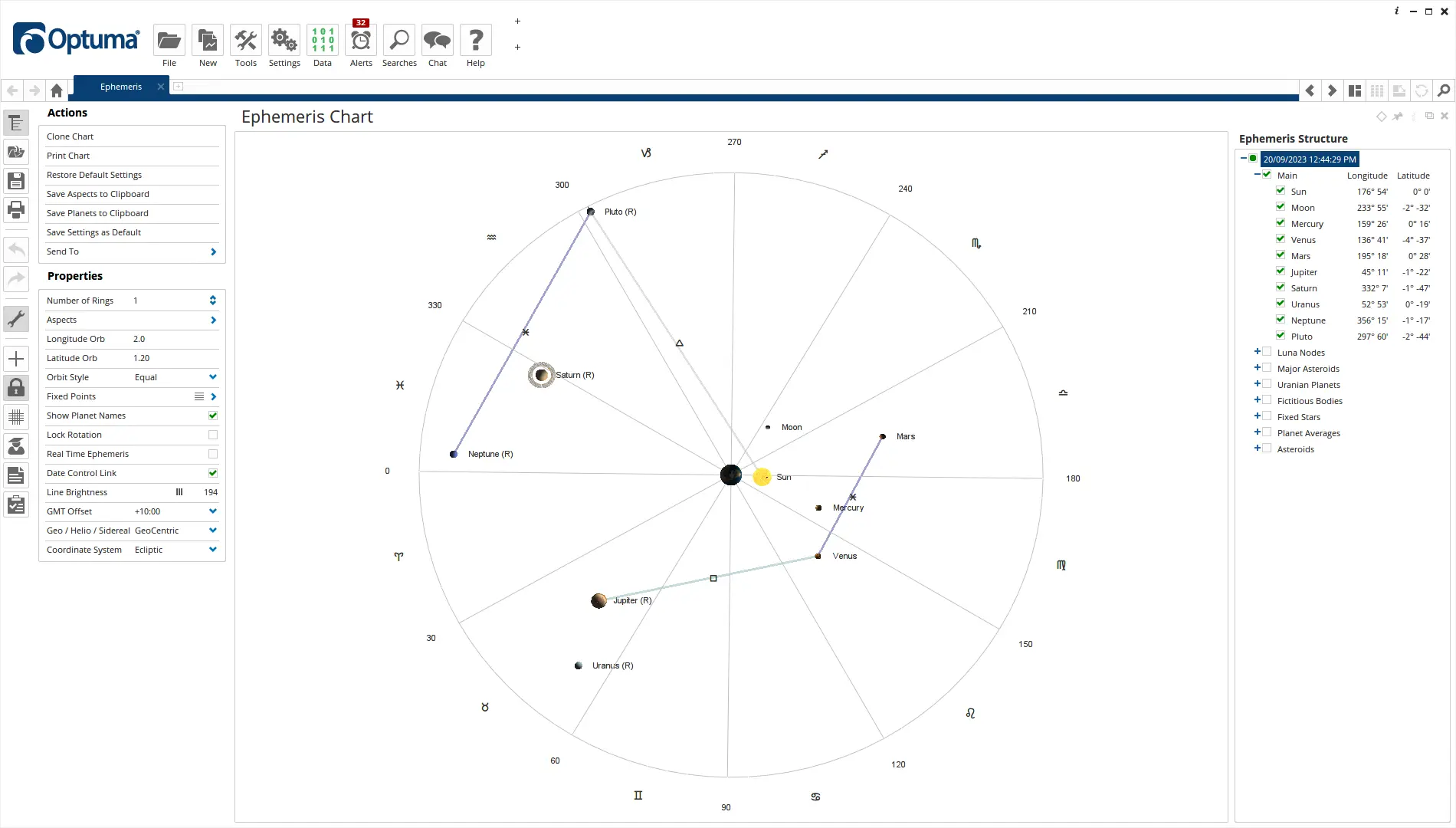

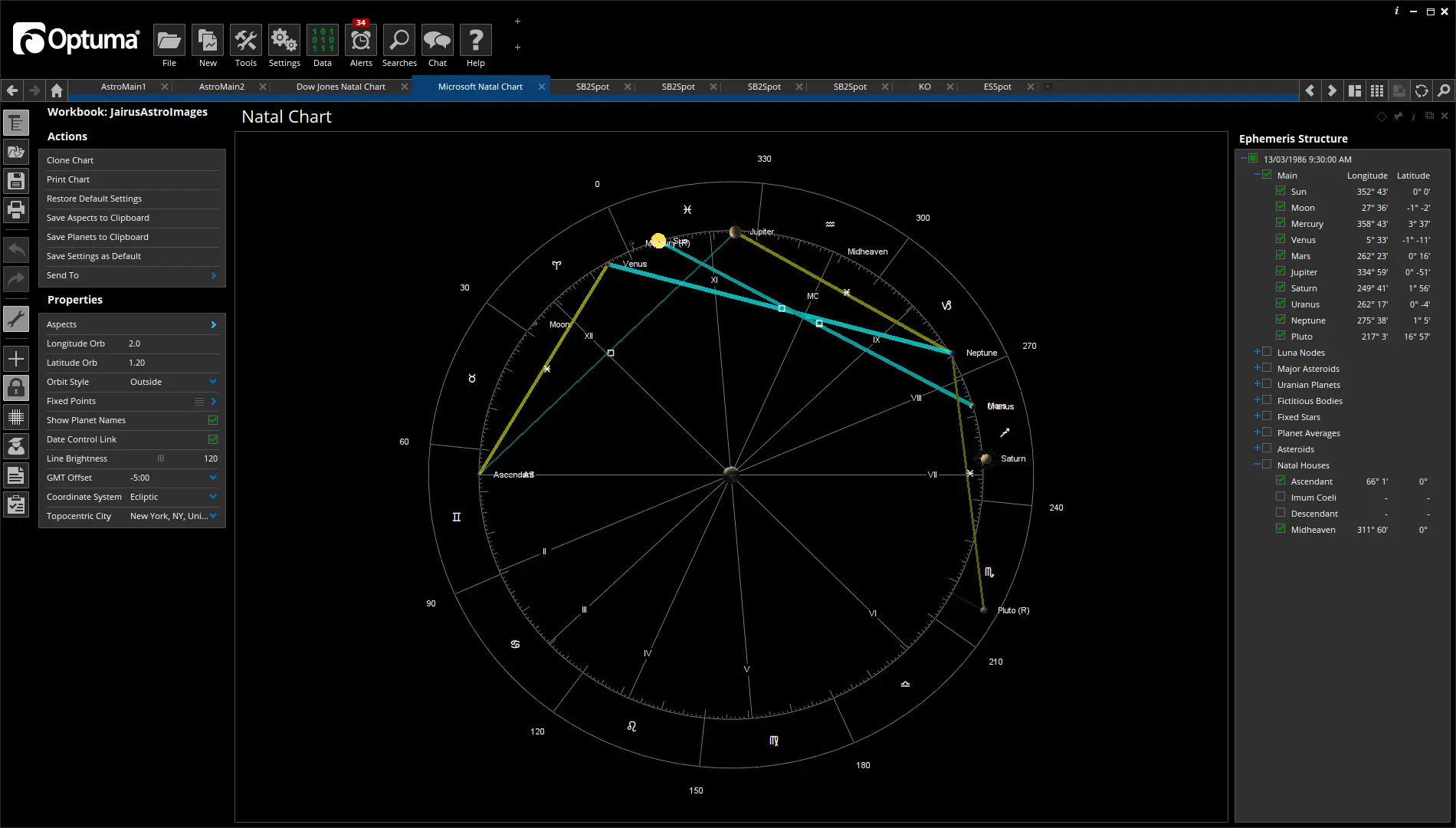

GannTrader uses the Swiss Ephemeris as the base for all calculations. This is a comprehensive library of calculations built on top of the NASA JPL ephemeris. Planet Positions, Houses, Aspects, and thousands of Asteroids are all available to be included in your analysis.

Available as a stand-alone chart and also as a mini-chart that can be placed on any price chart, the Ephemeris Chart allows you to view the exact planetary positions and aspects on any date.

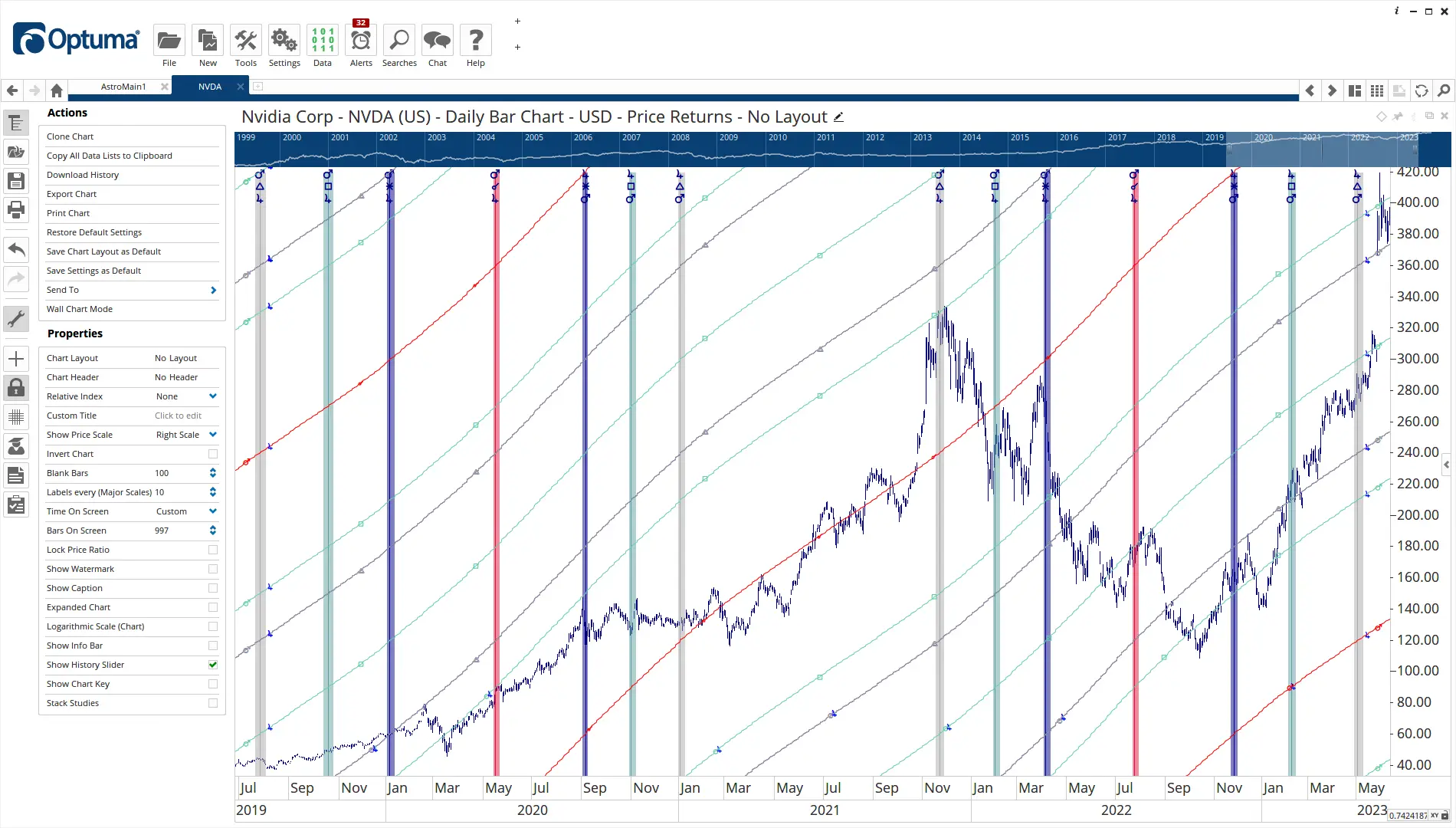

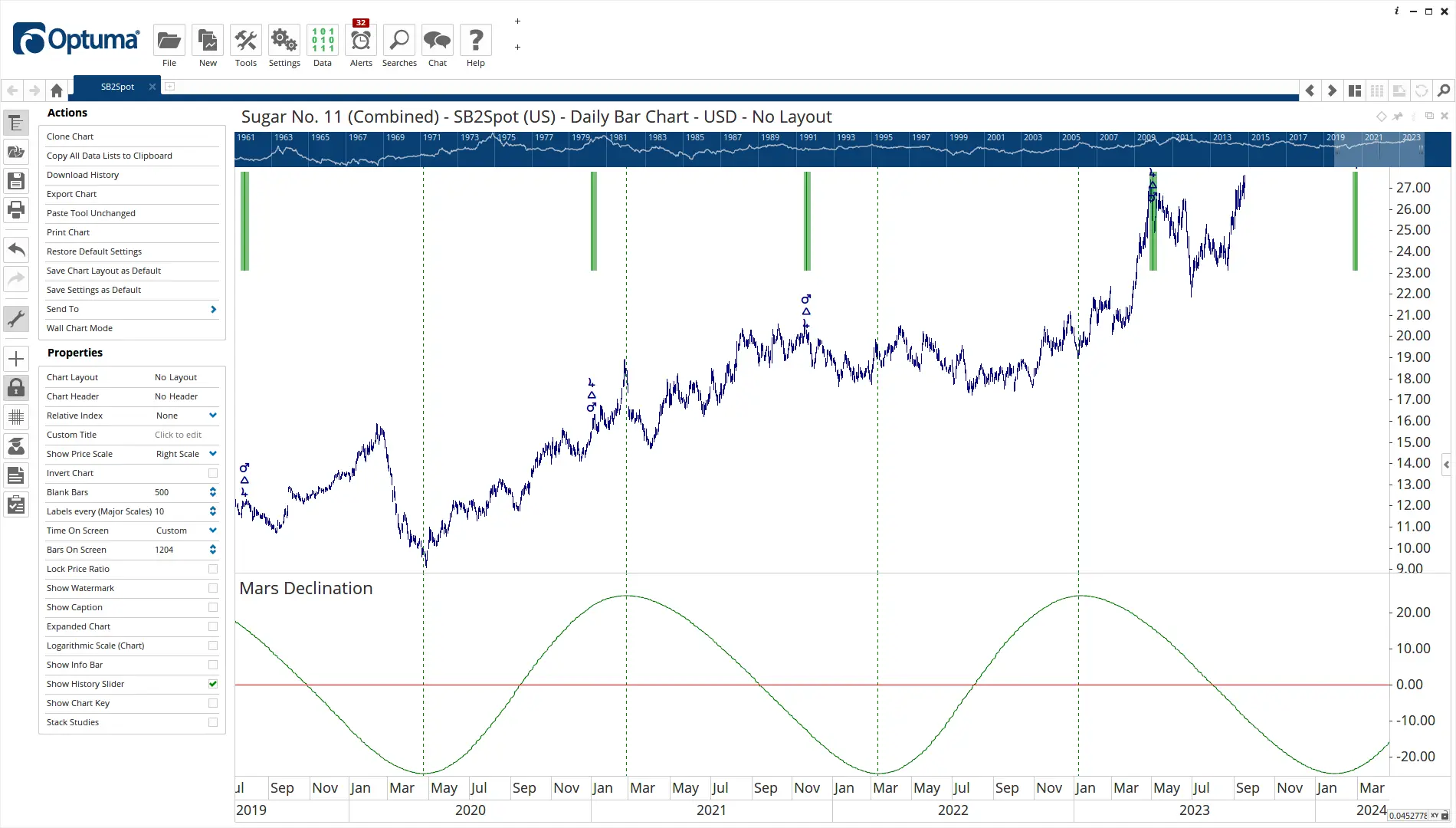

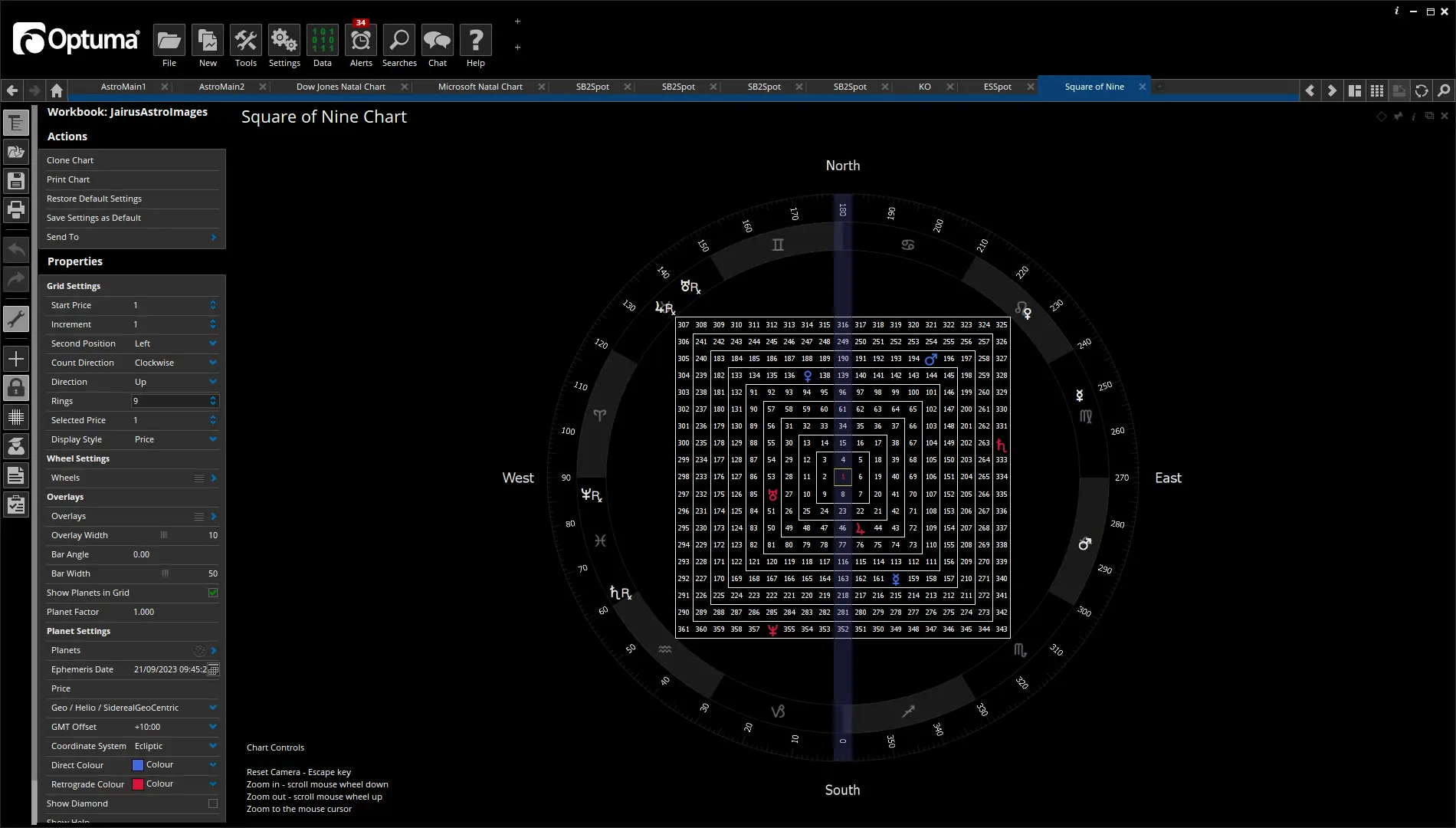

GannTrader has the standard wheel style chart and a unique Time series Ephemeris chart that maps out all the interactions between the planets.

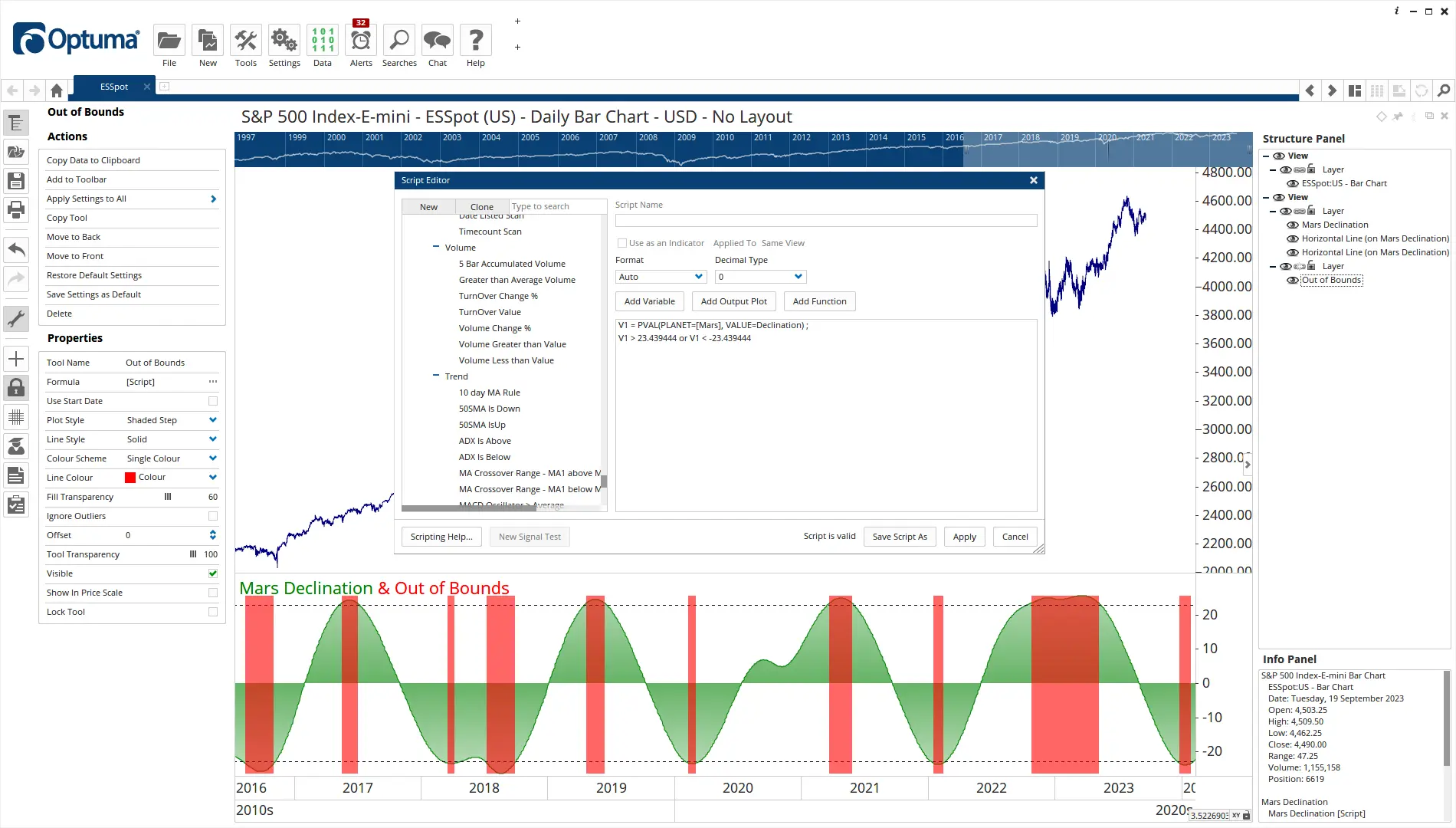

You are not limited to the Financial Astrology indicators in Gann Trader. Build your own signals and indicators using many of the same ephemeris building blocks unlocked in the Optuma scripting engine.

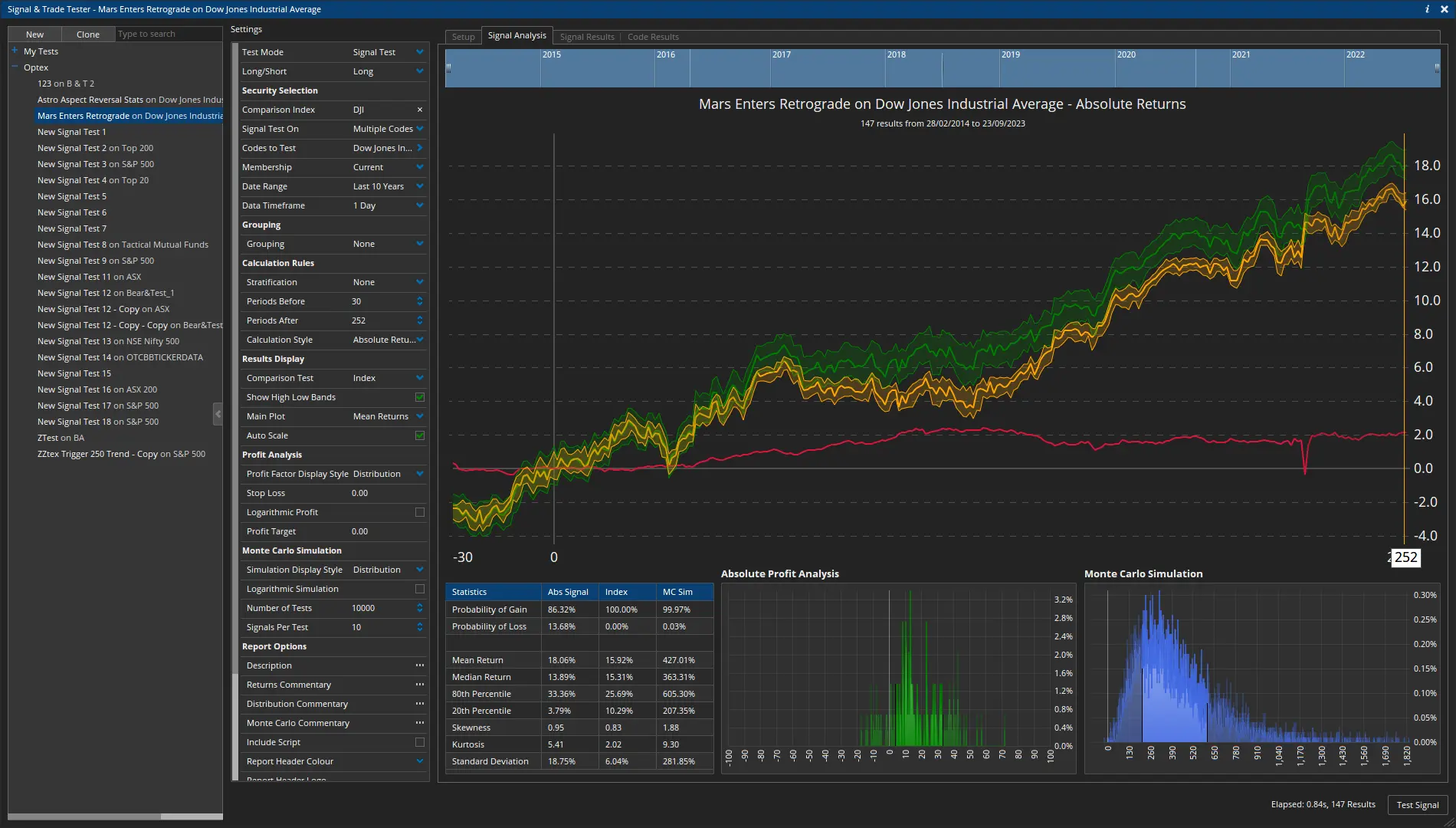

When GannTrader’s Financial Astrology tools are combined with Optuma’s quantitative analysis modules, you have a powerful application giving you full statistical analysis of Financial Astrology events. You can know the mean returns and standard deviations from any event that can be scripted in Optuma.

Financial astrology explores the relationship between celestial movements and financial markets. It applies astrological principles, such as planetary positions and aspects, to analyse and predict market trends, prices, and economic cycles.

Advocates of financial astrology believe planetary movements impact human behaviour, including financial decisions and market dynamics. They put forward that planetary alignments and astrological patterns can influence investor sentiment, market psychology, and overall market movements.

Financial astrologers employ various techniques and tools to interpret astrological data for financial analysis. This includes analysing planetary cycles, retrogrades, eclipses, and other astrological events to identify potential turning points or significant market trends.

Start your free trial today

View the markets with a clear lens Sign-up for your free trial of GannTrader

There is no need to know advanced mathematics to use our Gann & Astro tools. GannTrader does all the work for you. You will need a base understanding of Gann tools to implement them.

Yes. When you purchase our GannTrader package you get all the Astro tools currently available. You also get access to any new charts and tools added in the future.